Featured

Table of Contents

New Reporting Standards Forming the 2026 Financial Environment

The 2026 financial year has actually presented a series of shifts in how customer information is gathered and reported to the 3 significant bureaus. These modifications, driven by the 2026 Credit Transparency Act, concentrate on increasing the accuracy of files while providing customers with more control over their personal details. One of the most significant updates includes the treatment of medical financial obligation. As of early 2026, most paid medical collections have been wiped from reports completely, and unpaid medical financial obligations under a specific dollar threshold are no longer permitted to appear on customer files. This shift has offered instant relief to millions of individuals in Free Credit Counseling Session, allowing their ratings to show their present creditworthiness instead of previous health crises.

Another major change in 2026 concerns the combination of buy-now-pay-later (BNPL) data. For several years, these short-term installment loans operated in a gray area, typically going unreported unless a consumer defaulted. New 2026 guidelines now require these companies to report both favorable and unfavorable payment history to the bureaus. While this adds a layer of complexity to month-to-month tracking, it offers a method for those with thin credit files to develop history through small, workable purchases. For homeowners of the surrounding region, comprehending how these regular micro-loans affect a debt-to-income ratio is now a cornerstone of contemporary financial management.

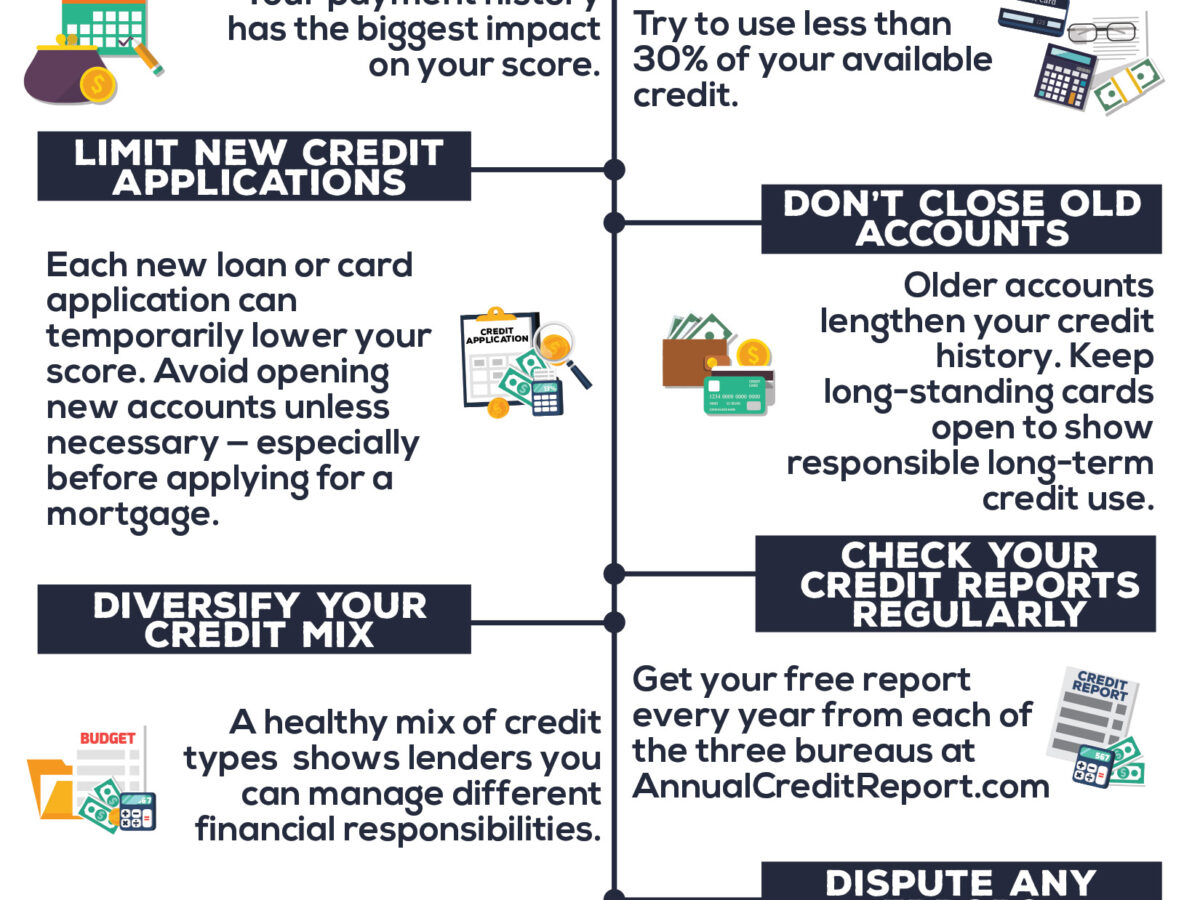

Recent advancements in Debt Relief recommend that reporting precision is the main motorist of score recovery in the current economy. Errors on credit reports remain a relentless concern, but the 2026 laws mandate a faster dispute resolution process. Lenders must now provide concrete proof of a debt within fifteen days of a disagreement, or the product must be eliminated. This puts the burden of proof squarely on the lenders, giving customers in the United States a more powerful position when challenging out-of-date or incorrect entries.

Reconstructing Credit in a High-Interest 2026 Economy

Rebuilding a credit profile in 2026 requires a different strategy than in previous years. Interest rates have stayed stubbornly high, making the expense of carrying a balance more costly than ever. Financial consultants suggest that the most effective method to improve a score now is through a combination of prompt payments and aggressive utilization decrease. In the domestic market, many individuals are turning to secured cards that offer graduated paths to unsecured lines of credit. These tools are specifically beneficial for those recovering from bankruptcy or extended periods of monetary instability.

Not-for-profit credit counseling companies have seen a surge in need as people browse these brand-new rules. These organizations, typically 501(c)(3) entities authorized by the Department of Justice, supply a neutral space for customers to assess their options. Experts who supply Professional Debt Relief Solutions highlight the requirement of combining high-interest responsibilities. A debt management program can be a lifeline in this environment, as it often involves negotiating with lenders to lower rate of interest and combine multiple monthly bills into a single payment. This structured approach helps make sure that no payments are missed, which is the single essential element in the 2026 credit history models.

For those living in Free Credit Counseling Session, regional neighborhood groups and banks typically partner with national nonprofits to offer workshops on these 2026 policies. Education is the very first line of defense versus predatory loaning practices that tend to multiply when traditional credit ends up being harder to gain access to. Knowing how to check out a 2026 credit disclosure form is now thought about a fundamental life skill, similar to basic tax preparation or home maintenance.

Mastering Individual Budgeting In The Middle Of 2026 Inflation

Budgeting in 2026 is no longer about just tracking expenditures-- it has to do with managing capital against unstable costs of living. Energy costs and housing costs in the local region have actually required numerous households to embrace "zero-based budgeting," where every dollar is assigned a particular task before the month starts. This technique avoids the "way of life creep" that can occur when small, recurring digital memberships go unnoticed. Specialists suggest using automated tools to sweep staying funds into high-yield cost savings accounts or towards high-interest debt at the end of every pay cycle.

House owners and prospective buyers are likewise dealing with distinct challenges. HUD-approved real estate therapy has actually ended up being an essential resource for those trying to go into the marketplace or remain in their homes. These therapists assist individuals comprehend the long-term ramifications of 2026 home mortgage products, a few of which function versatile payment structures that can be risky without appropriate assistance. House owners often look for Debt Management in Louisiana to ensure their home loan stays affordable under new 2026 interest rate caps and property tax adjustments.

The psychological element of budgeting is likewise gaining attention in 2026. Monetary tension is a leading reason for health concerns, and lots of counseling programs now consist of "financial health" parts. These programs teach consumers how to separate their self-respect from their credit rating, focusing rather on sustainable routines and long-lasting goals. In Free Credit Counseling Session, numerous independent affiliates of larger counseling networks provide these services totally free or at very low cost, ensuring that even those in deep monetary distress have access to professional aid.

Algorithmic Openness and the Future of Lending

As we move through 2026, the usage of expert system in financing choices has come under extreme scrutiny. New federal standards need lenders to be transparent about the "alternative information" they utilize to figure out credit reliability. This might include lease payments, utility expenses, and even constant savings patterns. For a consumer in the United States, this suggests that non-traditional monetary behaviors can lastly operate in their favor. However, it also implies that a single missed electrical expense might have a more pronounced result on a rating than it did five years back.

The 2026 economy rewards those who are proactive. Examining credit reports a minimum of as soon as a quarter has become the advised frequency, as the speed of data reporting has increased. Many customers now have access to real-time notifies through their banking apps, which can flag suspicious activity or unexpected score drops instantly. Benefiting from these technological tools, while keeping a relationship with a relied on not-for-profit counselor, supplies a balanced technique to monetary health.

Community-based financial literacy stays the most efficient way to guarantee long-term stability. Whether it is through a debt management program or a simple individually session with a certified therapist, the objective is the exact same: to move from a state of financial defense to among financial offense. By understanding the 2026 policies and mastering the art of the modern-day budget, people in Free Credit Counseling Session can safeguard their assets and construct a more safe and secure future no matter more comprehensive economic variations.

{kind=link}

Table of Contents

Latest Posts

How to Receive Better Combination Rates in Garden Grove Debt Consolidation Without Loans Or Bankruptcy

Conquering the Tension of Modern Financial Management

Remaining Ahead of the Curve With AI-Based Credit Tracking

More

Latest Posts

How to Receive Better Combination Rates in Garden Grove Debt Consolidation Without Loans Or Bankruptcy

Conquering the Tension of Modern Financial Management

Remaining Ahead of the Curve With AI-Based Credit Tracking